Pandemic Villains: Robinhood

Pandemic Villains: Robinhood

Have a pair of gangly Stanford grads built the perfect mousetrap?

As the world went into lockdown and the global economy into a spiral last spring, one company struck gold. A phone-based trading app called Robinhood began wiping the floor with more celebrated online brokerage rivals like Charles Schwab, TD Ameritrade, and E-Trade. The moment the pandemic began, it seemed, the world started trading stocks on Robinhood.

The numbers were staggering. Robinhood’s average daily trading volume tripled in the first quarter of this year, compared with the last quarter of 2019, and saw a tenfold increase in net deposits as millions were losing their jobs. The New York Times reported that the firm in the first quarter traded nine times as many shares as E-Trade, and an incredible 40 times as many as Schwab. It added 3 million new customer accounts, and by June was doing 4.3 million daily average revenue trades, or DARTS, more than any other online firm and more than Schwab and E-Trade combined.

Backed by a string of venture capital firms, including Kleiner Perkins, NEA, Sequoia, Thrive Capital, Ribbit Capital, and Google’s VC arm, GV, the firm received four major cash injections. Investors poured $200 million into the firm in April, $320 million more in July, another $200 million in August, and finally in November, another $460 million. Through this brief time, the company’s valuation jumped from $8.2 billion to $11.7 billion, by which time word leaked out that the firm had “asked banks to pitch for roles” for a possible IPO next year.

Analysts saw nothing but conquest ahead. “Competing versus Robinhood will be difficult,” said Larry Tabb, head of market structure research for Bloomberg Intelligence.

Robinhood seemed a new prodigal son of 21st-century capitalism, an awesome hybrid of Wall Street and Silicon Valley. The firm combined the pure greed of a Goldman, Sachs or JP Morgan Chase with the cheery, youth-friendly user-engagement strategies of Instagram or TikTok. The firm was founded in 2013 by two perma-smiling Stanford grads named Baiju Bhatt and Vlad Tenev, who wore khakis and Monkees haircuts and never seemed more than a moment away from bro-hugging one another.

These harmless-looking eggheads sounded genuinely excited to bring their product to the world, explaining they had a mission to “democratize finance for all.”

The app is perfectly designed for such “democratization.” It’s free, charging no commissions for trades. It also has an alluring, Joe Camel-like marketing campaign, featuring a host of bells and whistles in the form of free sample share giveaways, “scratch-off” rewards, and video confetti to celebrate transactions. “Even the most skeptical investor can be drawn in,” is how Jason Zweig of the Wall Street Journal just put it, describing how an assignment to learn more about the Robinhood experience led to something like addiction in less than a week.

Small-time customers who can’t afford a whole share of, say, Amazon stock can buy fractional stocks, and can also engage right away in complex options bets, just like the pros! What Bloomberg called “stock trading on a fun gamelike phone app” brings hordes of rookies into the markets: half of Robinhood’s customers this year were first-time traders, and 80% of its assets under management belong to millennials.

The firm is an icon of success in the pandemic age, finance’s answer to Netflix and Amazon Prime. Without sports to bet on, or bars to crawl, a whole new generation of “investors” are making Robinhood the destination for the ultimate new Covid-19 addiction: binge-trading. What could possibly go wrong with bringing more people into the stock market?

A lot, as it turns out. “Every time someone says they want to ‘democratize access,’” says Joe Saluzzi of Themis Trading, “I get very scared.”

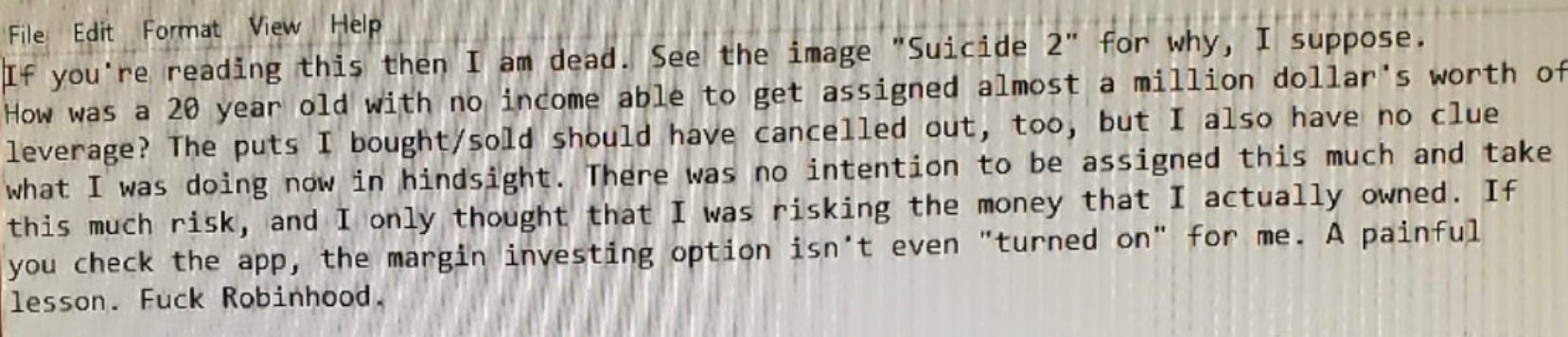

On June 12th, a 20-year-old University of Nebraska student named Alexander Kearns looked at his app and saw what he thought was a negative balance of $730,000. Misunderstanding the readout, which only showed part of a series of options trades he’d made, Kearns mistakenly believed he’d been ruined financially. He killed himself by stepping in front of a train, leaving behind a note asking, “How was a 20-year-old with no income able to get assigned almost a million dollar’s worth of leverage?”

Kearns appears to have been an otherwise happy young man. “At Thanksgiving, I could leave my kids with Alex, and he’d entertain them all day while I talked to his Dad,” says Bill Brewster, a relative. “He was a great kid.”

Brewster says the last time he talked to Alex was in March. “The sad thing is, he was really excited about finance, and for the right reasons. It wasn’t just about money. He was really interested in how it all works.”

The death of Kearns prompted predictable outrage, with critics focusing on a lack of controls and guidance for new users seeking to rush straight into complex trades, and, worse, a near-total absence of human customer service options. The Consumer Financial Protection Bureau database has many complaints from customers claiming an inability to contact the firm in timely fashion. If you have an urgent question, like for instance thinking you owe three-quarters of a million dollars, too bad: Robinhood’s chief feedback option is email, with response times of up to a week.

The company says that “while historically we’ve found we can best serve customers over email,” it’s also “exploring new channels for critical issues.” In the meantime, however, email those questions.

“All the other companies have people you can call,” says Brewster.

Soon, observers began asking deeper questions. Why is the company so game for customers to get into options trades? Why the emphasis on young, inexperienced users? How does a company that doesn’t charge fees make money?

The last question is key. In what the press accounts describe euphemistically using terms like a “controversial but legal practice,” Robinhood makes the bulk of its money on “payment for order flow.” It sells its data to high-frequency traders like Citadel and Virtu, market makers who ostensibly are paying for the honor of executing trades for Robinhood investors. These firms, using the technology that’s the subject of the celebrated Michael Lewis book Flash Boys, hunt out tiny price differences and gauge market sentiment and supply and demand before other traders, using sophisticated algorithms to jump ahead of the pack.

A Robinhood investor typing in a trade is just beginning a series of transactions that might result in a string of actors being compensated. Robinhood does not and can not post orders directly to exchanges like the NASDAQ; for a fee, it sends all of its orders to market maker firms like Citadel or Virtu. Those firms in turn have what amounts to a free option on the Robinhood trader’s order. They can execute the trade themselves, or they can offload it to an exchange, which in turn posts the order and compensates the market maker firm in the form of rebates, while earning money itself by charging fees for “data feed” that include information about such retail orders.

The mechanics of all of this are not absolutely necessary for Robinhood customers to understand, but it is worth asking the question of whether all of these actors in between the Robinhood client and his or her trades withdraw more or less value than, say, traditional broker fees. The HFT firms that handle the bulk of Robinhood’s business have always maintained that what they do is socially beneficial, because their trades “add liquidity” and make markets more efficient. Critics say the opposite, that high-speed algorithmic trading is just using advance peeks at market intelligence to turn trading into a low-risk arbitrage-like activity.

At any rate, “payment for order flow” isn’t unique to Robinhood. E-Trade, Schwab, and others also do it. Because it’s not clear in all cases how purchasers use their information, it’s hard sometimes to make a concrete determination about the ethics of these transactions. In the case of Robinhood, however, three facts are worth noting:

Whatever HFT firms are paying for order flow, it’s worth it to them financially. If they’re paying 50 cents for your trade, they’re making more than 50 cents.

Robinhood is getting gargantuan sums for its flow. In the first quarter of 2020, firms like Citadel, Virtu, and Wolverine paid them $91 million. In the second quarter, that number jumped to $180 million.

These firms pay more significantly more for Robinhood’s order flow than they do for the order flow of other firms: an average of 17% more, according to a Bloomberg analysis.

One might add a few other details, like that Tenev and Bhatt, prior to founding Robinhood, designed algorithmic software for high-frequency traders. As Saluzzi puts it, “these guys know how the plumbing works.”

Also, Robinhood’s compensation model differs from E-Trade and other firms. As an analysis by the investment bank Piper Sandler put it this summer, “Robinhood receives a fixed rate per spread (vs. a fixed rate per share by the other eBrokers).” Rather than receiving simple payment by volume, Robinhood receives a percentage of the spread between the bid and the ask in each trade.

This is interesting because while HFT proponents insist their practices narrow spreads, some critics maintain that high-frequency trading ends up widening spreads. In Saluzzi’s book “Broken Markets,” for instance, he estimates that while spreads are narrower in “perhaps 5% of the most actively traded names,” they’re wider in “the other 95% of the market.”

A cynical person might take all this in and hypothesize that engineers trained in building high-frequency trading software could reverse-engineer a retail stock-trading app that would serve two purposes. On the one hand, it would provide sophisticated traders with the most valuable kind of order flow in the form of inexperienced “dumb money” investors, while designing a compensation model best equipped to take advantage of how HFT traders operate.

Robinhood obviously has a different take on all of these issues. It argues, and market maker firms agree, that the primary reason it’s paid more for its flow than other firms has to do with the relatively small size of its customers’ trades. “For a market maker,” the firm told TK, “executing a smaller order is lower risk compared to a 10,000 share order, which is baked into the compensation model.” In other words, a firm like Citadel or Wolverine would rather deal with a kid in Oklahoma trading a hundred shares out of his basement, as opposed to an experienced broker that might dangle one small trade, but be backed by enough money to impact the market in unpredictable ways with the next one. The Robinhood investor, they say, is just safer business.

Whatever you believe about the efficacy of commission-free trading, the revenue potential of a phone-based trading app marketed to millennials in the middle of a pandemic is obvious. As the New York Times and others reported, one of Robinhood’s investors is the actor Ashton Kutcher, who attended a Zoom meeting for the firm in June. In that meeting, he reportedly gushed about the company’s potential by comparing it to gambling websites. Kutcher put out a statement that he was “not insinuating that Robinhood is a gambling platform,” but rather referring to the company’s “current growth metrics.”

Robinhood says the same thing, that it built its platform to “make investing more accessible to a new generation and to make first-time investors into long-term investors.” Adding, “it’s important to distinguish between accessible, modern design and gamification,” the company insists its research shows that over time, “most of our customers use a buy-and-hold strategy.”

Brewster isn’t buying it. “Everything is designed to make investing look like DraftKings,” he says. Moreover, the company’s practice of offering push notifications when customers’ stocks move up or down 5% or 10% could trigger an endless cycle of dopamine-generating responses, combining FOMO/clickbait psychology with the betting urge. Customers think, “if it’s down, I gotta get out. If it’s up, I gotta buy more,” says Brewster.

The obvious problem is that a lot of these younger customers have no clue what they’re doing. “Retail investors don’t understand stocks, let alone options,” sighs Saluzzi. He compares the service to bringing amateur poker players to Vegas and seating them not at a table with old ladies and tourists, but with the best players in town. “It’s throwing them right in with the sharks,” he says.

Even some of the firm’s detractors are conflicted, however, not wanting to argue against anyone’s freedom to jump in the deep end right away. Some take an even more positive view. Barry Ritholtz, author of Bailout Nation and Chairman and Chief Investment Officer of Ritholtz Wealth Management, thinks Robinhood is just the modern incarnation of the original online trading platforms that became pop culture hits by similarly promising to “democratize” brokerage.” He recalls the famed “Let’s light this candle” ads for Ameritrade in the nineties:

Ritholtz thinks Robinhood is great, so long as young investors are fully prepared to get decked in the face. It’s crucial, he says, that they only risk “fun money,” and enter into the activity being comfortable with their balance going to zero. There may even be value in that, he says.

“If they get their asses handed to them, that’s a lesson that’s much better to learn early in life than later,” Ritholtz says. He adds that some talent might even rise from the Robinhood ranks. “A handful of people will discover, ‘Hey, I can hit a three-point jumper,’” is how he puts it.

It’s often speculated that part of Robinhood’s success is that it appeals to a millennial demographic that, because of a shrinking economy, is politically concerned with the question of whether or not it can or will have any stake in the future. “They have more of an ownership mentality than my generation did,” Ritholtz says. “It’s, ‘I want to be a partner in the upside of the economics of society.’”

Which is great, he thinks, although he and other old-school investors do worry what will happen to Robinhood’s customers when the markets go down. “It’s been famously said, ‘Never confuse a bull market with brains,’” he says, noting the S&P 500 is up nearly 64% since lows on March 23, right around the time the Robinhood’s numbers began zooming skyward.

Others are more pessimistic. “This isn’t going to end well,” is how one investment advisor puts it. “There are tons of these new investors who think they’re doing great, but they’re like Wile E. Coyote — probably off the cliff already, but thanks to the Fed, they just haven’t gone splat yet.”

Robinhood is under investigation by the SEC, ostensibly for failure to fully disclose its practice of selling order flow. The Wall Street Journal said last month the firm “could have to pay a fine exceeding $10 million,” which doesn’t sound like much given the amount of money the firm has already made, and the El Dorado it still stands to win in a potential IPO. Robinhood was also fined by the Financial Industry Regulatory Authority (FINRA) last year for failure to abide by “best execution” rules, which require member firms to take reasonable measures to find the best prices for customers.

If and when IPO money comes, Robinhood will be on its way to becoming a finance version of Facebook: a free platform that keeps a sea of customers engaged with a hyper-stimulating user experience, while making money selling intelligence about those customers’ behaviors to expert wealth extractors on the other end.

It’s the perfect mousetrap, among other things because of its name. “That’s the other thing,” says Brewster. “They call it Robin Hood.” Instead of stealing from the rich and giving to the poor, the American version takes in the young and sells them to computer-powered hedge funds; this Robin Hood is the house that always wins. If there’s a more brilliant metaphor for capitalism in the Covid age, it’s hard to imagine.

The saying goes if the service is free, you are the product.

Whenever a young kid on my portfolio team (I worked on Wall Street for years) would say to me, "this is kind of like gambling" I'd always reply, "No, IS gambling, and the sooner you understand that the better you will be at this."

The insane urge to get rich overnight, without having to actually work for it, has ruined many a man over the centuries. Market speculation is America's favorite past time.

From the article: -- “It’s been famously said, ‘Never confuse a bull market with brains,’” he says, noting the S&P 500 is up nearly 64% since lows on March 23, right around the time the Robinhood’s numbers began zooming skyward."

Robinhood is just riding a wave of cheap credit, greed and stupidity. They are not the cause of the massive asset inflation this year.

On March 13, the Federal Reserve announced that it was slashing borrowing rates (for the Big Banks, not for you) to zero again, and resuming "Quantitative Easing," its gargantuan asset purchase program (of securities from banks at inflated prices, not from you.)

There's the real villain.